KFF Health News' 'What the Health?': Countdown to Shutdown

The Host

Julie Rovner

KFF Health News

Julie Rovner is chief Washington correspondent and host of KFF Health News’ weekly health policy news podcast, “What the Health?” A noted expert on health policy issues, Julie is the author of the critically praised reference book “Health Care Politics and Policy A to Z,” now in its third edition.

Health and other federal programs are at risk of shutting down, at least temporarily, as Congress races toward the Oct. 1 start of the fiscal year without having passed any of its 12 annual appropriations bills. A small band of conservative House Republicans are refusing to approve spending bills unless domestic spending is cut beyond levels agreed to in May.

Meanwhile, former President Donald Trump roils the GOP presidential primary field by vowing to please both sides in the divisive abortion debate.

This week’s panelists are Julie Rovner of KFF Health News, Alice Miranda Ollstein of Politico, Rachel Cohrs of Stat News, and Tami Luhby of CNN.

Panelists

Alice Miranda Ollstein

Politico

Rachel Cohrs

Stat News

Tami Luhby

CNN

Among the takeaways from this week’s episode:

- The odds of a government shutdown over spending levels are rising. While entitlement programs like Medicare would be largely spared, past shutdowns have shown that closing the federal government hobbles things Americans rely on, like food safety inspections and air travel.

- In Congress, the discord isn’t limited to spending bills. A House bill to increase price transparency in health care melted down before a vote this week, demonstrating again how hard it is to take on the hospital industry. Legislation on how pharmacy benefit managers operate is also in disarray, though its projected government savings means it could resurface as part of a spending deal before the end of the year.

- On the Senate side, legislation intended to strengthen primary care is teetering under Bernie Sanders’ stewardship — in large part over questions about how to pay for it. Also, this week Democrats broke Alabama Republican Sen. Tommy Tuberville’s abortion-related blockade of military promotions (kind of), going around him procedurally to confirm the new chair of the Joint Chiefs of Staff.

- And some Republicans are breaking with abortion opponents and mobilizing in support of legislation to renew the United States President’s Emergency Plan for AIDS Relief — including the former president who spearheaded the program, George W. Bush. Meanwhile, polling shows President Joe Biden is struggling to claim credit for the new Medicare drug negotiation program.

- And speaking of past presidents, former President Donald Trump gave NBC an interview over the weekend in which he offered a muddled stance on abortion. Vowing to settle the long, inflamed debate over the procedure — among other things — Trump’s comments were strikingly general election-focused for someone who has yet to win his party’s nomination.

Plus, for “extra credit,” the panelists suggest health policy stories they read this week that they think you should read, too:

Julie Rovner: The Washington Post’s “Inside the Gold Rush to Sell Cheaper Imitations of Ozempic,” by Daniel Gilbert.

Alice Miranda Ollstein: Politico’s “The Anti-Vaccine Movement Is on the Rise. The White House Is at a Loss Over What to Do About It,” by Adam Cancryn.

Rachel Cohrs: KFF Health News’ “Save Billions or Stick With Humira? Drug Brokers Steer Americans to the Costly Choice,” by Arthur Allen.

Tami Luhby: CNN’s “Supply and Insurance Issues Snarl Fall Covid-19 Vaccine Campaign for Some,” by Brenda Goodman.

Also mentioned in this week’s episode:

- The AP’s “Biden’s Medicare Price Negotiation Is Broadly Popular. But He’s Not Getting Much Credit,” by Seung Min Kim and Linley Sanders.

- Roll Call’s “Sanders, Marshall Reach Deal on Health Programs, but Challenges Remain,” by Jessie Hellmann and Lauren Clason.

CLICK TO EXPAND THE TRANSCRIPT

Transcript: Countdown to Shutdown

[Editor’s note: This transcript was generated using both transcription software and a human’s light touch. It has been edited for style and clarity.]

Julie Rovner: Hello and welcome back to “What the Health?” I’m Julie Rovner, chief Washington correspondent for KFF Health News. And I’m joined by some of the best and smartest health reporters in Washington. We’re taping this week on Thursday, Sept. 21, at 9 a.m. because, well, lots of news this week. And as always, news happens fast, and things might well have changed by the time you hear this. So here we go. We are joined today via video conference by Tami Luhby of CNN.

Tami Luhby: Good morning.

Rovner: Rachel Cohrs of Stat News.

Rachel Cohrs: Hi, everybody.

Rovner: And Alice Miranda Ollstein of Politico.

Alice Miranda Ollstein: Hello.

Rovner: Let’s get to some of that news. We will begin on Capitol Hill, where I might make a T-shirt from this tweet from Wednesday from longtime congressional reporter Jake Sherman: “I feel like this is not the orderly appropriations process that was promised after the debt ceiling deal passed.” For those of you who might’ve forgotten, many moons ago, actually it was May, Congress managed to avoid defaulting on the national debt, and as part of that debt ceiling deal agreed to a small reduction in annual domestic spending for the fiscal year that starts Oct. 1 (as in nine days from now). But some of the more conservative Republicans in the House want those cuts to go deeper, much deeper, in fact. And now they’re refusing to either vote for spending bills approved by the Republican-led appropriations committee or even for a short-term spending bill that would keep the government open after this year’s funding runs out. So how likely is a shutdown at this point? I would hazard a guess to say pretty likely. And anybody disagree with that?

Ollstein: It’s more likely than it was a week or two ago, for sure. The fact that we’re at the point where the House passing something that they know is dead on arrival in the Senate would be considered a victory for them. And so, if that’s the case, you really have to wonder what the end game is.

Rovner: Yeah, I mean it was notable, I think, that the House couldn’t even pass the rule for the Defense Appropriations Bill, which is the most Republican-backed spending bill, and the House couldn’t get that done. So I mean it does not bode well for the fate of some of these domestic programs that Republicans would, as I say, like to cut a lot deeper. Right?

Cohrs: Democrats are happy, I think, to watch Republicans flail for a while. I think we saw this during the speaker votes. Obviously, a CR [continuing resolution] could pass with wide bipartisan support, but I think there’s a political interest for Democrats going into an election year next year to lean into the idea of the House Republican chaos and blaming them for a shutdown. So I wouldn’t be too optimistic about Democrats billing them out anytime soon.

Rovner: But, bottom line, of course, is that a shutdown is not great for Democrats who support things that the government does. I mean, Tami, you’re watching, what does happen if there’s a shutdown? Not everything shuts down and not all the money stops flowing.

Luhby: No, and the important thing, unlike in the debt ceiling, potentially, was that Social Security will continue, Medicare will continue, but it’ll be very bothersome to a lot of people. There’ll be important things that … potentially chaos at airlines and food safety inspectors. I mean some of them are sometimes considered essential workers, but there’s still issues there. So people will be mad because they can’t go to their national parks potentially. I mean it’s different every time, so it’s a little hard to say exactly what the effects will be and we’ll see also whether this will be a full government shutdown, which will be much more serious than a partial government shutdown, although at this point it doesn’t look like they’re going to get any of the appropriation bills through.

Rovner: I was going to say, yeah, sometimes when they get some of the spending bills done, there’s a partial shutdown because they’ve gotten some of the spending bills done, but I’m pretty sure they’ve gotten zero done now. I think there’s one that managed to pass both the House and the Senate, but basically this would be a full shutdown of everything that’s funded through the appropriations process. Which as Tami points out, the big things are the Smithsonian and the National Zoo close, and national parks close, but also you can’t get an awful lot of government services. Meanwhile, the ill will among House Republicans is apparently rubbing off on other legislation. The House earlier this week was supposed to vote on a relatively noncontroversial package of bills aimed at making hospital insurance and drug prices more transparent, among other things. But even that couldn’t get through. Rachel, what happened to the transparency bill that everybody thought was going to be a slam-dunk?

Cohrs: Well, I don’t think everybody thought it was going to be a slam-dunk given the chaos that we saw, especially in the Democratic Caucus last week, where one out of three chairmen who work on health care in the House endorsed the package, but the other two would not. And they ran into a situation where, with the special rule that they were using to consider the House transparency package, they needed two-thirds vote to pass and they couldn’t get enough Democrats on board to pass it. And I think there were some process concerns from both sides that there was a compromise that came out right after August recess and it hadn’t been socialized properly and they didn’t have their ducks in a row in the Democratic side. But ultimately, I mean, the big picture for me I think was how hard it really is to take on the hospital industry. Because this was the first real effort I think from the House and it melted down before its first vote. That doesn’t mean it’s dead yet, but it was an embarrassment, I think, to everyone who worked on this that they couldn’t get this pretty noncontroversial package through. And when I tried to talk to people about what they actually oppose, it was these tiny little details about a privacy provision or one transparency provision and not with the big idea. It wasn’t ideological necessarily. So I think it was just a reflection on Congress has taken on pharma, they’re working on PBMs this year, but if they really do want to tackle hospital costs, which are a very big part of Medicare spending, it’s going to be a tough road ahead for them.

Rovner: As we like to point out, every single member of Congress has a hospital in their district, and they are quick to let their members of Congress know what they want and how they want them to vote on things. Before we move on, where are we on the PBM legislation? I know there was a whole raft of hearings this week on doing something about PBMs. And my inbox is full of people from both sides. “The PBMs are making drug prices higher.” “No, the PBMs are helping keep drug prices in check.” Where are we with the congressional effort to try and at least figure out what the PBMs do?

Cohrs: Yeah, I think there is still some disarray at this point. I would watch for action in December or whenever we actually have a conversation about government funding because some of these PBM bills do save money, which is the golden ticket in health care because there are a lot of programs that need to be paid for this year. So Congress will continue to debate those over the next couple of weeks, but I think everyone that I talk to is expecting potential passage in a larger package at the end of the year.

Rovner: So speaking of things that need to be paid for, the saga of Sen. Bernie Sanders and the reauthorization of some key primary care programs, including the popular community health center program, continues. When we left off last July, Sen. Sanders, who chairs the Senate Health, Education, Labor & Pensions Committee [HELP], tried to advance a bill to extend and greatly expand primary care programs without negotiating with his ranking Republican on the committee, Louisiana Sen. Bill Cassidy, who had his own bill to renew the programs. Cassidy protested and blocked the bill’s movement and the whole enterprise came to a screeching halt. Last week, Sanders announced he’d negotiated a bipartisan bill, but not with Cassidy, rather with Kansas Republican Roger Marshall, who chairs the relevant subcommittee. Cassidy, however, is still not pleased. Rachel, you’re following this. Sanders has scheduled a markup of the bill for later today. Is it really going to happen?

Cohrs: Well, I think things are on track and the thing to remember about a markup is it passes on a majority. So as long as Sen. Sanders can keep his Democratic members in line and gets Sen. Marshall, then it can pass committee. But I think there are some concerns that other Republicans will share with Sen. Cassidy about how the bill is paid for. There are a lot of ambitious programs to expand workforce training, have debt forgiveness, and address the primary care workforce crisis in a more meaningful way. But the list of pay-fors is a little undisciplined from what I’ve seen, I would say.

Rovner: That’s a good word.

Cohrs: Sen. Sanders is pulling some pay-fors from other committees, which he can’t necessarily do by himself, and they don’t actually have estimates from the Congressional Budget Office for some of the pay-fors that they’re planning to use. They’re just using internal committee math, which I don’t think is going to pass muster with Republicans in the full Senate, even if it gets through committee today. So I think we’ll see some of those concerns flare up. It could get ugly today compared with HELP markups of the past of community health center bills. And there are certainly some concerns about the application of the Hyde Amendment too, and how it would apply to some of this funding as it moves through the appropriations process.

Rovner: That’s the amendment that bans direct government funding of abortion, and there’s always a fight about the Hyde Amendment, which are reauthorizing these health programs. But I mean, we should point out, I mean this is one of the most bipartisanly popular programs, both the community health center program and these programs that basically give federal money to train more primary care doctors, which the country desperately needs. I mean, it’s something that pretty much everybody, or most of Congress, supports, but Cassidy has what, 60 amendments to this bill. I guess he’s really not happy. Cassidy who supports this in general just is unhappy with this process, right?

Cohrs: I think his concern is more that the legislation is half-baked, not that he’s against the idea of it. And Sen. Cassidy did sign on to a more limited House proposal as well, just saying, we need to fund the community health centers, we need to do something. This isn’t ready for prime time. We could see further negotiations, but the time is ticking for this funding to expire.

Rovner: Well, another program whose authorization expires at the end of the month is PEPFAR, the international AIDS/HIV program. It’s being blocked by anti-abortion activists among others, even though it doesn’t have anything to do with the abortion. And this is not just a bipartisan program, it’s a Republican-led program. Former President George W. Bush who signed it into law in 2003, had an op-ed this week pushing for the program in The Washington Post. Alice, you’ve been following this one. Is there any progress on PEPFAR?

Ollstein: Yes and no. There’s not a vote scheduled, there’s not a “Kumbaya” moment, but we are seeing some movement. I call it “Establishment Republican Strike Back.” You have some both on- and off-the-Hill Republicans really mobilizing to say, “Look, we need to reauthorize this program. This is ridiculous.” And they’re going against the anti-abortion groups and their allies on Capitol Hill who say, “No, let’s just extend this program just year by year through appropriations, not a reauthorization.” Which they say would rubber-stamp the Biden administration redirecting money towards abortion, which the Biden administration and everybody else denies is happening. And so we confirmed that Chairman Mike McCaul in the House and Lindsey Graham in the Senate are working with Democrats on some sort of reauthorization bill. It might not be the full five years, it might be three years, we don’t really know yet. But they think that at least a multiyear reauthorization will give the program some stability rather than the one-year funding patch that other House Republicans are mulling. So we’re going to see where this goes; obviously, it’s an interesting test for the influence of these anti-abortion groups on Capitol Hill. And my colleague and I also scooped that former President Bush, who oversaw the creation of this program, is quietly lobbying certain members, having meetings, and so we will see what kind of pull he still has in the party.

Rovner: Well, this was one of his signature achievements, literally. So it’s something that I know that … and we should point out, unlike the spending bills, the appropriation bills, if this doesn’t happen by Oct. 1, nothing stops, it’s just it becomes theoretically unauthorized, like many programs are, and it’s considered not a good sign for the program.

Luhby: One thing I also wanted to just bring up quickly, tangentially related to health care, but also showing how bipartisan programs are not getting the support that they did, is the WIC program, which is food assistance for women, infants and children, needs more money. Actually participation is up, but even before that, the House Republicans wanted to cut the funding for it, and that was going to be a big divide between them and the Senate. And now because participation is up, the Biden administration is actually asking for another $1.4 billion for the program. This is a program that, again, has always had support and has been fully funded, not had to turn people away. And now it’s looking that many women and small children may not be able to get the assistance if Congress isn’t able to actually fund the program fully.

Rovner: Yes, they’re definitely tied in knots. Well, Oct. 1 turns out to be a key date for a lot of health care issues. It’s also the day drugmakers are supposed to notify Medicare whether they will participate in negotiations for the 10 high-cost drugs Medicare has chosen for the first phase of the program that Congress approved last year. But that might all get blocked if a federal judge rules in favor of a suit brought by the U.S. Chamber of Commerce, among others. Rachel, there was a hearing on this last week, where does this lawsuit stand and when do we expect to hear something from the judge?

Cohrs: So the judge didn’t ask any questions of the attorneys, so they were essentially presenting arguments that we’ve already seen previewed in some of the briefing materials. We are expecting some action by Oct. 1, which is when the Chamber had requested a ruling on whether there’s going to be a preliminary injunction, just because drugmakers are supposed to sign paperwork and submit data to CMS by that Oct. 1 date. So I think we are just waiting to see what the ruling might be. Some of the key issues or whether the Chamber actually has standing to file this lawsuit, given it’s not an actual drug manufacturer. And there was some quibbling about what members they listed in the lawsuit. And then I think they only addressed the argument that the negotiation program violated drugmakers’ due process rights, which isn’t the full scope of the lawsuit. It’s not an indicator of success really anywhere else, but it is important because it is the very first test. And if a preliminary injunction is issued, then it brings everything to a halt. So I think it would be very impactful for other drugmakers as well.

Rovner: Nobody told me when I became a health reporter that I was going to have to learn every step of the civil judicial process, and yet here we are. Well, while we are still on the subject of drug prices, a new poll from the AP and the NORC finds that while the public, Republicans and Democrats, still strongly support Medicare being able to negotiate the price of prescription drugs, President [Joe] Biden is getting barely any credit for having accomplished something that Democrats have been pushing for for more than 20 years. Most respondents in the survey either don’t think the plan goes far enough, because, as we point out, it’s only the first 10 drugs, or they don’t realize that he’s the one that helped push it over the finish line. This should have been a huge win and it’s turning out to be a nothing. Is that going to change?

Ollstein: It’s kind of a “Groundhog Day” of the Obamacare experience in which they pass this big, huge reform that people had been fighting for so long, but they’re trying to campaign on it when people aren’t really feeling the effects of it yet. And so when people aren’t really feeling the benefit and they’re hearing, “Oh, we’re lowering your drug prices.” But they’re going to the pharmacy and they’re paying the same very high amount, it’s hard to get a political win from that. The long implementation timeline is against them there. So there are some provisions that kick in more quickly, so we’ll have to see if that makes any kind of difference. I think that’s why you hear them talk a lot about the insulin price cap because that is already in effect, but that hits fewer people than the bigger negotiation will theoretically hit eventually. So it’s tough, and I think it leaves a vacuum where the drug industry and conservatives can fearmonger or raise concerns and say, “This will make drugs inaccessible and they won’t submit new cures for approval.” And all this stuff. And because people aren’t feeling the benefits, but they’re hearing those downsides, yeah, that makes the landscape even tougher for Democrats.

Luhby: This is very much the pattern that the Biden administration has had with a lot of its achievements or successes because it’s also not getting any credit for anything in the economy. The job market is relatively strong still, the economy is relatively strong. Yes, we have high inflation and high prices, even though that’s moderated, prices are still high, and that’s what people are seeing. Gas prices are now up again, which is not good for the administration. But they’re touting their Bidenomics, which also includes lowering drug prices. But generally polling shows, including our CNN polling shows, that people do not think the economy is doing well and they’re not giving Biden any credit for anything.

Cohrs: I think part of the problem is that … it’s different from the Affordable Care Act where it was health care, health care, health care for a very long time. This is lumped into a bill called the Inflation Reduction Act. I think it got lumped in with climate, got looped in with tax. And the media, we did our best, but it was hard to explain everything that was in the bill. And Medicare negotiation is complicated, it’s wonky, and I don’t know that people fully understood everything that was in the Inflation Reduction Act when it passed and they capitulated to Sen. [Joe] Manchin for what he wanted to name it. And so I think some of that got muddled when it first passed and they’re kind of trying to do catch-up work to explain, again, like Alice said, something that hasn’t gone into effect, which is a really tough uphill climb.

Rovner: This has been a continuing frustration for Democrats, which is that actually getting legislation done in Washington always involves some kind of compromise, and it’s always going to be incremental. And the public doesn’t really respond to things that are incremental. It’s like, “Why isn’t it bigger? Why didn’t they do what they promised?” And so the Republicans get more credit for stopping things than the Democrats get for actually passing things. Right. Well, let us turn to abortion. The breaking news today is that the Senate is finally acting to bust the blockade Alabama Republican Sen. Tommy Tuberville has had on military promotion since February to protest a Defense Department policy allowing service people leave to travel to other states for abortions. And Tuberville himself is part of this breakage, right, Alice? And it’s not a full breakage.

Ollstein: Right. And there have also been some interesting interviews that maybe raise questions on how much Tuberville understands the mechanics of what he’s doing because he said in an interview, “Oh, well, the people who were in these jobs before, they’ll just stay in it and it’s fine.” And they had to explain, “Well, statutorily, they can’t after a certain date.” And he seemed surprised by that. And now you’re seeing these attempts to go around his own blockade, and Democrats to go around his blockade. In part, for a while, Democrats were really not wanting to do that, schedule these votes, until he fully relented because they thought that would increase the pressure.

Rovner: They didn’t want to do it nomination by nomination for the big-picture ones because they were afraid that would leave behind the smaller ones.

Ollstein: Exactly. But this is dragging on so long that I think you’re seeing some frustration and desire to do something, even if it’s not fully resolving the standoff.

Rovner: And I’m seeing frustration from other Republicans. Again, the idea of a Republican holding up military promotions for six months is something that was not on my Republican Bingo card five years ago or even two years ago. I’m sure he’s not making a lot of his colleagues very happy with this. So on the Republican presidential campaign trail, abortion continues to be a subject all the candidates are struggling with — all of them, it seems, except former President Donald Trump, who said in an interview with NBC on Sunday that he alone can solve this. Francis, you have the tape.

Donald Trump: We are going to agree to a number of weeks or months or however you want to define it, and both sides are going to come together, and both sides, and this is a big statement, both sides will come together and for the first time in 52 years, you’ll have an issue that we can put behind us.

Rovner: OK. Well, Trump — who actually seemed all over the place about where he is on the issue in a fairly bald attempt to both placate anti-abortion hardliners in the party’s base and those who support abortion rights, whose votes he might need if he wants to win another election — criticized his fellow Republicans, who he called, “inarticulate on the subject.” I imagine that’s not going over very well among all of the other Republican candidates, right?

Ollstein: We have a piece up on this this morning. One, Trump is clearly acting like he has already won the primary, so he is trying to speak to a general audience, as you noted, and go after those votes in the middle that he may need and so he’s pitching this compromise. And we have a piece that the anti-abortion groups are furious about this, but they don’t really know what to do about it because he probably is going to be the nominee and they’re probably going to spend tens of millions to help elect him if he is, even though they’re furious with these comments he’s making. And so it’s a really interesting moment for their influence. Of course, Trump is trying to have it both ways, he also is calling himself the most pro-life president of all time. He is continually taking credit for appointing the justices to the Supreme Court who overturned Roe v. Wade.

Rovner: Which he did.

Ollstein: Exactly.

Rovner: Which is true.

Ollstein: Which he definitely did. But he is not toeing the line anymore that these groups want. These groups want him to endorse some sort of federal ban on abortion and they want him to praise states like Florida that have passed even stricter bans. He is not doing that. And so there’s an interesting dynamic there. And now his primary opponents see this as an opening, they’re trailing him in the polls, and so they’re trying to capitalize on this. [Gov. Ron] DeSantis and a bunch of others came out blasting him for these abortion remarks. But again, he’s acting like he’s already won the primary, he’s brushing it off and ignoring them.

Rovner: I love how confident he is though, that there’s a way to settle this — really, that there is a compromise, it’s just nobody’s been smart enough to get to it.

Ollstein: Well, he also, in the same interview, he said he’ll solve the Ukraine-Russia war in a day. So I mean, I think we should consider it in that context. It was interesting when I talked to all these different anti-abortion groups, they all said the idea of cutting some sort of deal is ludicrous. There is no magic deal that everybody would be happy about. If anything …

Rovner: And those on the other side will say the same thing.

Ollstein: Exactly. How could you watch what’s happened over the past year or 30 years and think that’s remotely possible? However, they did acknowledge that him saying that does appeal to a certain kind of voter, who is like, “Yeah, let’s just compromise. Let’s just get past this. I’m sick of all the fighting.” So it’s another interesting tension.

Rovner: Yeah. And I love how Trump always says the quiet part out loud, which is that this is not a great issue for Republicans and they’re not talking about it right. It’s like Republicans know this is a not-great issue for Republicans, but they don’t usually say that in an interview on national television. That is Trump, and this will continue. Well, finally this week I wanted to talk about what I am calling the dark underbelly of the new weight loss drugs. This is my extra credit this week. It’s a Washington Post story by Daniel Gilbert called “Inside the Gold Rush to Sell Cheaper Imitations of Ozempic.” It’s about the huge swell of sometimes not-so-legitimate websites and wellness spas selling unapproved formulations of semaglutide and tirzepatide — better known by their brand names Ozempic, Wegovy, and Mounjaro — to unsuspecting consumers because the demand for these diabetes drugs is so high for people who want to lose weight. The FDA has declared semaglutide at least to be in shortage for the people it was originally approved for, those with Type 2 diabetes. But that designation legally allows compounding pharmacies to manufacture their own versions, at least in some cases, except to quote the piece, “Since then, a parallel marketplace with no modern precedent has sprung up attracting both licensed medical professionals and entrepreneurs with histories ranging from regulatory violations to armed robbery.” Meanwhile, and this is coming from a separate story, both Eli Lilly and Novo Nordisk, the manufacturers of the approved versions of the drugs, are suing companies they say are selling unapproved versions of their drug, including, in some cases, drugs that actually pretend to be the brand name drug that aren’t. This is becoming really a big messy buyer-beware market, right? Rachel, you guys have written about this.

Cohrs: It has. Yeah, my colleagues have done great coverage, including I think the lawsuit by manufacturers of these drugs who are seeing their profits slipping through their fingers as patients are turning to these alternatives that aren’t necessarily approved by the FDA. And I think there are also risks because we have seen some side effects from these medications; they range from some very serious GI symptoms to strange dreams. There’s just a whole lot going on there. And I think it is concerning that some patients are getting ahold of these medications, which are expensive if you’re buying them the traditional way. And again, for weight loss, I think some of these medications are still off-label, they’re not FDA-approved. So if they’re getting these without any supervision from a medical provider or somebody who they can ask when they have questions that come up and are monitoring for some of these other side effects, then I think it is a very dangerous game for these patients. And I think it’s just a symptom of this outpouring of interest and the regulators’, I think, failure to keep up with it. And there’s also some supply concerns. So I think it’s just this perfect storm of desperation from patients and the bureaucracy struggling to keep up.

Rovner: Yeah. One of the reasons I chose the story is I really feel like this is unprecedented. I mean, I suppose it could have been predicted because these drugs do seem to be very good at what they do and they are very expensive and very hard to get, so not such a surprise that not-so-honest people might spring up to try and fill the void. But it’s still a little bit scary to see people selling heaven only knows what to people who are very anxious to take things.

Luhby: And in related news, there are more doctors who are interested in obesity medicine now, so everyone is trying to cash in.

Rovner: Yeah, I mean, eventually I imagine this will sort itself out. It’s just that at the beginning when it’s so popular, although I will still … I keep thinking this, is the solution to really throw this much money at it or to try to figure out how to make these drugs cheaper? If it’s going to be such a societal good, maybe we should do something about the price. Anyway, that is my extra credit in this week’s news. Now we will take a quick break and then we’ll come back with the rest of our extra credits.

Hey, “What the Health?” listeners, you already know that few things in health care are ever simple. So, if you like our show, I recommend you also listen to “Tradeoffs,” a podcast that goes even deeper into our costly, complicated, and often counterintuitive health care system. Hosted by longtime health care journalist and friend Dan Gorenstein, “Tradeoffs” digs into the evidence and research data behind health care policies and tells the stories of real people impacted by decisions made in C-suites, doctors’ offices, and even Congress. Subscribe wherever you listen to your podcasts.

OK, we are back and it’s time for our extra-credit segment. That’s when we each recommend a story we read this week we think you should read, too. As always, don’t worry if you miss it; we will post the links on the podcast page at kffhealthnews.org and in our show notes on your phone or other mobile device. Tami, why don’t you go first this week?

Luhby: Sure. Well, this week I chose a good story by one of my colleagues, Brenda Goodman. It’s titled “Supply and Insurance Issues Snarl Fall Covid-19 Vaccine Campaign for Some.” And we’ve all been hearing this, I heard this from a friend of mine who’s a doctor, we know Cynthia Cox at KFF tweeted about this. And that even though the new vaccines are ready and the Biden administration has been pushing people to go get them, and many people are eager to get them, they’re not so easy to get. Either because drugstores are running out, that’s what happened to my friend. She went in and said there just wasn’t any supply available. Or for some other people, they’re supposed to be free for most Americans, but the insurance companies haven’t caught up with that yet. So they go in and either they’re denied or the pharmacy tells them that they have to pay potentially $200 for the vaccines. So the problem here is that there’s already an issue with getting vaccines and people getting vaccinated in this country and then putting up extra hurdles for them will only cause more problems and cause fewer people to get vaccinated because some people may not come back.

Rovner: Talk about something that should have been predictable. The distributors knew it was going to be available and pretty much when, and the insurance companies knew it was going to be available and pretty much when, and yet somehow they seem to have not gotten their act together when the predictable surge of people wanting to get the vaccine early came about. Alice, you wanted to add something?

Ollstein: Just anecdotally, the supply and the demand are completely out of whack. My partner is back home in Alabama right now and he was at a pharmacy where they were just wandering around asking random people, “Will you take the shot? Will you take the shot?” And a bunch of people were saying, “No.” And meanwhile, here in D.C., myself and everyone I know is just calling around wanting to get it and not able to. And so you think we’d have figured this out better after so many years of this.

Rovner: Well, I have an appointment for tomorrow. We’ll see if it happens. Rachel, why don’t you go next?

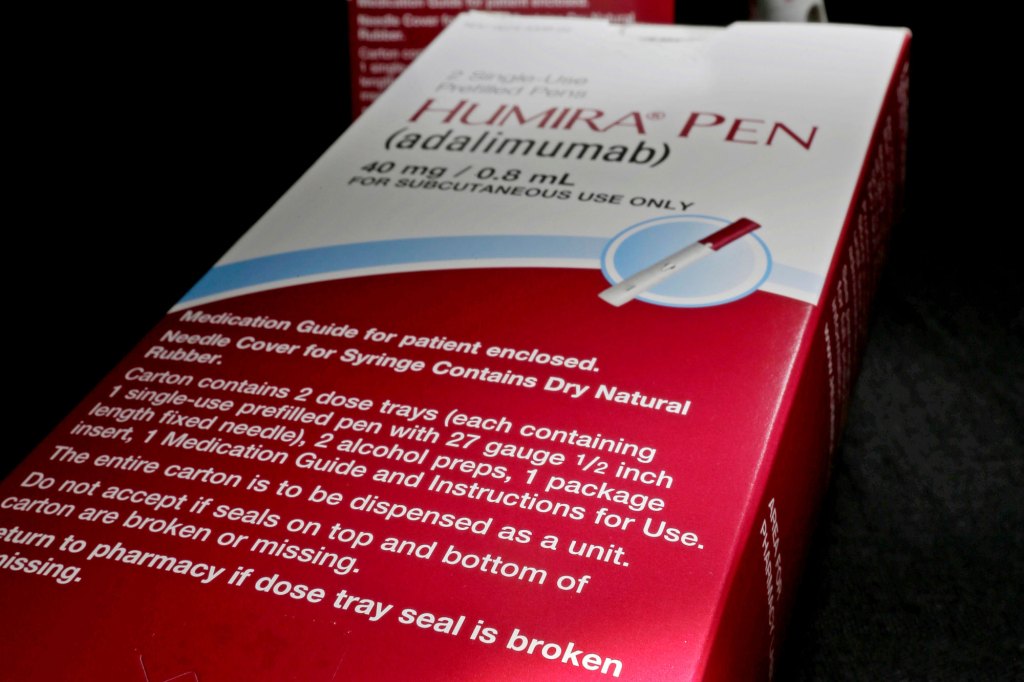

Cohrs: Sure. I chose a KFF Health News story by Arthur Allen, and the headline is “Save Billions or Stick With Humira? Drug Brokers Steer Americans to the Costly Choice.” And I just love a story where it’s off the news cycle a little bit and we see this big splashy announcement. And I think Arthur did a great job of following up here and seeing what actually was happening with formulary placement for Humira and the new biosimilars that just came on the market.

Rovner: Yep. Remind us what Humira is?

Cohrs: Oh, yeah. So it’s one of the most profitable drugs ever. The company that makes it, AbbVie, had created this big patent thicket to try to prevent it from competition for a very long time, but this year saw competition that had been on the market in Europe finally come online in the U.S. So again, a big change for AbbVie, for the market. But I think there was concern about whether people would actually switch to these new medications that have lower prices. But again, as it gets caught up and spit out of our drug supply chain, there are a whole lot of incentives that don’t necessarily result in the cheaper medication being prescribed. And Arthur found that Express Scripts and Optum, which are two of the three biggest pharmacy benefit managers, have the biosimilar versions of Humira at the same price as Humira. So that doesn’t really create a lot of incentive for people to switch. So I think it was just great follow-up reporting and we don’t really have a lot of visibility into these formularies sometimes. So I think it was a illuminating piece.

Rovner: Yeah. And the mess that is drug pricing. Alice.

Ollstein: So I also chose a great piece by my colleague Adam Cancryn and it’s called “The Anti-Vaccine Movement Is on the Rise. The White House Is at a Loss Over What to Do About It.” It’s part of a series we’re doing on anti-vax sentiment and its impacts. And this is just going into how the Biden administration really doesn’t have a plan for combating this, even as it’s posing a bigger and bigger public health threat. And some of their attempts to go after misinformation online were stymied in court and they also are struggling with not wanting to elevate it by debunking it — that that age-old tension of, is it better to just ignore it or is it better to combat it directly? A lot of this is also tying into RFK Jr.’s presidential bid and how much to acknowledge that or not. But the impact is that they’re not really taking this on, even as it’s getting worse and worse in the country.

Rovner: And I got a bunch of emails this week about the anti-vax movement spreading to pets — that people are now resisting getting their dogs and cats vaccinated. Seriously. I mean, it is a serious problem. Obviously, if people stop getting rabies vaccines, that could be a big deal. So something else to watch. All right. Well, I already did my extra credit. So that is it for this week. As always, if you enjoy the podcast, you can subscribe wherever you get your podcasts. We’d appreciate it if you left us a review; that helps other people find us, too. Special thanks as always to our indefatigable engineer, Francis Ying. Also, as always, you can email us your comments or questions. We’re at whatthehealth@kff.org. Or you can tweet me; I’m still @jrovner on X and on Bluesky. Tami?

Luhby: You can tweet me at @Luhby. I sometimes check it still.

Rovner: Rachel.

Cohrs: I’m on X @rachelcohrs.

Rovner: Alice.

Ollstein: I’m @AliceOllstein.

Rovner: We will be back in your feed next week. Until then, be healthy.

Credits

Francis Ying

Audio producer

Emmarie Huetteman

Editor

To hear all our podcasts, click here.

And subscribe to KFF Health News’ “What the Health?” on Spotify, Apple Podcasts, Pocket Casts, or wherever you listen to podcasts.

KFF Health News is a national newsroom that produces in-depth journalism about health issues and is one of the core operating programs at KFF—an independent source of health policy research, polling, and journalism. Learn more about KFF.

USE OUR CONTENT

This story can be republished for free (details).

2 years 1 month ago

Elections, Health Care Costs, Health Industry, Medicaid, Medicare, Multimedia, Pharmaceuticals, Public Health, Abortion, Biden Administration, Drug Costs, HIV/AIDS, KFF Health News' 'What The Health?', Podcasts, U.S. Congress, Women's Health

Save Billions or Stick With Humira? Drug Brokers Steer Americans to the Costly Choice

Tennessee last year spent $48 million on a single drug, Humira — about $62,000 for each of the 775 patients who were covered by its employee health insurance program and receiving the treatment. So when nine Humira knockoffs, known as biosimilars, hit the market for as little as $995 a month, the opportunity for savings appeared ample and immediate.

But it isn’t here yet. Makers of biosimilars must still work within a health care system in which basic economics rarely seems to hold sway.

For real competition to take hold, the big pharmacy benefit managers, or PBMs, the companies that negotiate prices and set the prescription drug menu for 80% of insured patients in the United States, would have to position the new drugs favorably in health plans.

They haven’t, though the logic for doing so seems plain.

Humira has enjoyed high-priced U.S. exclusivity for 20 years. Its challengers could save the health care system $9 billion and herald savings from the whole class of drugs called biosimilars — a windfall akin to the hundreds of billions saved each year through the purchase of generic drugs.

The biosimilars work the same way as Humira, an injectable treatment for rheumatoid arthritis and other autoimmune diseases. And countries such as the United Kingdom, Denmark, and Poland have moved more than 90% of their Humira patients to the rival drugs since they launched in Europe in 2018. Kaiser Permanente, which oversees medical care for 12 million people in eight U.S. states, switched most of its patients to a biosimilar in February and expects to save $300 million this year alone.

Biologics — both the brand-name drugs and their imitators, or biosimilars — are made with living cells, such as yeast or bacteria. With dozens of biologics nearing the end of their patent protection in the next two decades, biosimilars could generate much higher savings than generics, said Paul Holmes, a partner at Williams Barber Morel who works with self-insured health plans. That’s because biologics are much more expensive than pills and other formulations made through simpler chemical processes.

For example, after the first generics for the blockbuster anti-reflux drug Nexium hit the market in 2015, they cost around $10 a month, compared with Nexium’s $100 price tag. Coherus BioSciences launched its Humira biosimilar, Yusimry, in July at $995 per two-syringe carton, compared with Humira’s $6,600 list price for a nearly identical product.

“The percentage savings might be similar, but the total dollar savings are much bigger,” Holmes said, “as long as the plan sponsors, the employers, realize the opportunity.”

That’s a big if.

While a manufacturer may need to spend a few million dollars to get a generic pill ready to market, makers of biosimilars say their development can require up to eight years and $200 million. The business won’t work unless they gain significant market share, they say.

The biggest hitch seems to be the PBMs. Express Scripts and Optum Rx, two of the three giant PBMs, have put biosimilars on their formularies, but at the same price as Humira. That gives doctors and patients little incentive to switch. So Humira remains dominant for now.

“We’re not seeing a lot of takeup of the biosimilar,” said Keith Athow, pharmacy director for Tennessee’s group insurance program, which covers 292,000 state and local employees and their dependents.

The ongoing saga of Humira — its peculiar appeal to drug middlemen and insurers, the patients who’ve benefited, the patients who’ve suffered as its list price jumped sixfold since 2003 — exemplifies the convoluted U.S. health care system, whose prescription drug coverage can be spotty and expenditures far more unequal than in other advanced economies.

Biologics like Humira occupy a growing share of U.S. health care spending, with their costs increasing 12.5% annually over the past five years. The drugs are increasingly important in treating cancers and autoimmune diseases, such as rheumatoid arthritis and inflammatory bowel disease, that afflict about 1 in 10 Americans.

Humira’s $200 billion in global sales make it the best-selling drug in history. Its manufacturer, AbbVie, has aggressively defended the drug, filing more than 240 patents and deploying legal threats and tweaks to the product to keep patent protections and competitors at bay.

The company’s fight for Humira didn’t stop when the biosimilars finally appeared. The drugmaker has told investors it doesn’t expect to lose much market share through 2024. “We are competing very effectively with the various biosimilar offerings,” AbbVie CEO Richard Gonzalez said during an earnings call.

How AbbVie Maintains Market Share

One of AbbVie’s strategies was to warn health plans that if they recommended biosimilars over Humira they would lose rebates on purchases of Skyrizi and Rinvoq, two drugs with no generic imitators that are each listed at about $120,000 a year, according to PBM officials. In other words, dropping one AbbVie drug would lead to higher costs for others.

Industry sources also say the PBMs persuaded AbbVie to increase its Humira rebates — the end-of-the-year payments, based on total use of the drug, which are mostly passed along by the PBMs to the health plan sponsors. Although rebate numbers are kept secret and vary widely, some reportedly jumped this year by 40% to 60% of the drug’s list price.

The leading PBMs — Express Scripts, Optum, and CVS Caremark — are powerful players, each part of a giant health conglomerate that includes a leading insurer, specialty pharmacies, doctors’ offices, and other businesses, some of them based overseas for tax advantages.

Yet challenges to PBM practices are mounting. The Federal Trade Commission began a major probe of the companies last year. Kroger canceled its pharmacy contract with Express Scripts last fall, saying it had no bargaining power in the arrangement, and, on Aug. 17, the insurer Blue Shield of California announced it was severing most of its business with CVS Caremark for similar reasons.

Critics of the top PBMs see the Humira biosimilars as a potential turning point for the secretive business processes that have contributed to stunningly high drug prices.

Although list prices for Humira are many times higher than those of the new biosimilars, discounts and rebates offered by AbbVie make its drug more competitive. But even if health plans were paying only, say, half of the net amount they pay for Humira now — and if several biosimilar makers charged as little as a sixth of the gross price — the costs could fall by around $30,000 a year per patient, said Greg Baker, CEO of AffirmedRx, a smaller PBM that is challenging the big companies.

Multiplied by the 313,000 patients currently prescribed Humira, that comes to about $9 billion in annual savings — a not inconsequential 1.4% of total national spending on pharmaceuticals in 2022.

The launch of the biosimilar Yusimry, which is being sold through Mark Cuban’s Cost Plus Drugs pharmacy and elsewhere, “should send off alarms to the employers,” said Juliana Reed, executive director of the Biosimilars Forum, an industry group. “They are going to ask, ‘Time out, why are you charging me 85% more, Mr. PBM, than what Mark Cuban is offering? What is going on in this system?’”

Cheaper drugs could make it easier for patients to pay for their drugs and presumably make them healthier. A KFF survey in 2022 found that nearly a fifth of adults reported not filling a prescription because of the cost. Reports of Humira patients quitting the drug for its cost are rife.

Convenience, Inertia, and Fear

When Sue Lee of suburban Louisville, Kentucky, retired as an insurance claims reviewer and went on Medicare in 2017, she learned that her monthly copay for Humira, which she took to treat painful plaque psoriasis, was rising from $60 to $8,000 a year.

It was a particularly bitter experience for Lee, now 81, because AbbVie had paid her for the previous three years to proselytize for the drug by chatting up dermatology nurses at fancy AbbVie-sponsored dinners. Casting about for a way to stay on the drug, Lee asked the company for help, but her income at the time was too high to qualify her for its assistance program.

“They were done with me,” she said. Lee went off the drug, and within a few weeks the psoriasis came back with a vengeance. Sores covered her calves, torso, and even the tips of her ears. Months later she got relief by entering a clinical trial for another drug.

Health plans are motivated to keep Humira as a preferred choice out of convenience, inertia, and fear. While such data is secret, one Midwestern firm with 2,500 employees told KFF Health News that AbbVie had effectively lowered Humira’s net cost to the company by 40% after July 1, the day most of the biosimilars launched.

One of the top three PBMs, CVS Caremark, announced in August that it was creating a partnership with drugmaker Sandoz to market its own cut-rate version of Humira, called Hyrimoz, in 2024. But Caremark didn’t appear to be fully embracing even its own biosimilar. Officials from the PBM notified customers that Hyrimoz will be on the same tier as Humira to “maximize rebates” from AbbVie, Tennessee’s Athow said.

Most of the rebates are passed along to health plans, the PBMs say. But if the state of Tennessee received a check for, say, $20 million at the end of last year, it was merely getting back some of the $48 million it already spent.

“It’s a devil’s bargain,” said Michael Thompson, president and CEO of the National Alliance of Healthcare Purchaser Coalitions. “The happiest day of a benefit executive’s year is walking into the CFO’s office with a several-million-dollar check and saying, ‘Look what I got you!’”

Executives from the leading PBMs have said their clients prefer high-priced, high-rebate drugs, but that’s not the whole story. Some of the fees and other payments that PBMs, distributors, consultants, and wholesalers earn are calculated based on a drug’s price, which gives them equally misplaced incentives, said Antonio Ciaccia, CEO of 46Brooklyn, a nonprofit that researches the drug supply chain.

“The large intermediaries are wedded to inflated sticker prices,” said Ciaccia.

AbbVie has warned some PBMs that if Humira isn’t offered on the same tier as biosimilars it will stop paying rebates for the drug, according to Alex Jung, a forensic accountant who consults with the Midwest Business Group on Health.

AbbVie did not respond to requests for comment.

One of the low-cost Humira biosimilars, Organon’s Hadlima, has made it onto several formularies, the ranked lists of drugs that health plans offer patients, since launching in February, but “access alone does not guarantee success” and doesn’t mean patients will get the product, Kevin Ali, Organon’s CEO, said in an earnings call in August.

If the biosimilars are priced no lower than Humira on health plan formularies, rheumatologists will lack an incentive to prescribe them. When PBMs put drugs on the same “tier” on a formulary, the patient’s copay is generally the same.

In an emailed statement, Optum Rx said that by adding several biosimilars to its formularies at the same price as Humira, “we are fostering competition while ensuring the broadest possible choice and access for those we serve.”

Switching a patient involves administrative costs for the patient, health plan, pharmacy, and doctor, said Marcus Snow, chair of the American College of Rheumatology’s Committee on Rheumatologic Care.

Doctors’ Inertia Is Powerful

Doctors seem reluctant to move patients off Humira. After years of struggling with insurance, the biggest concern of the patient and the rheumatologist, Snow said, is “forced switching by the insurer. If the patient is doing well, any change is concerning to them.” Still, the American College of Rheumatology recently distributed a video informing patients of the availability of biosimilars, and “the data is there that there’s virtually no difference,” Snow said. “We know the cost of health care is exploding. But at the same time, my job is to make my patient better. That trumps everything.”

“All things being equal, I like to keep the patient on the same drug,” said Madelaine Feldman, a New Orleans rheumatologist.

Gastrointestinal specialists, who often prescribe Humira for inflammatory bowel disease, seem similarly conflicted. American Gastroenterological Association spokesperson Rachel Shubert said the group’s policy guidance “opposes nonmedical switching” by an insurer, unless the decision is shared by provider and patient. But Siddharth Singh, chair of the group’s clinical guidelines committee, said he would not hesitate to switch a new patient to a biosimilar, although “these decisions are largely insurance-driven.”

HealthTrust, a company that procures drugs for about 2 million people, has had only five patients switch from Humira this year, said Cora Opsahl, director of the Service Employees International Union’s 32BJ Health Fund, a New York state plan that procures drugs through HealthTrust.

But the biosimilar companies hope to slowly gain market footholds. Companies like Coherus will have a niche and “they might be on the front end of a wave,” said Ciaccia, given employers’ growing demands for change in the system.

The $2,000 out-of-pocket cap on Medicare drug spending that goes into effect in 2025 under the Inflation Reduction Act could spur more interest in biosimilars. With insurers on the hook for more of a drug’s cost, they should be looking for cheaper options.

For Kaiser Permanente, the move to biosimilars was obvious once the company determined they were safe and effective, said Mary Beth Lang, KP’s chief pharmacy officer. The first Humira biosimilar, Amjevita, was 55% cheaper than the original drug, and she indicated that KP was paying even less since more drastically discounted biosimilars launched. Switched patients pay less for their medication than before, she said, and very few have tried to get back on Humira.

Prescryptive, a small PBM that promises transparent policies, switched 100% of its patients after most of the other biosimilars entered the market July 1 “with absolutely no interruption of therapy, no complaints, and no changes,” said Rich Lieblich, the company’s vice president for clinical services and industry relations.

AbbVie declined to respond to him with a competitive price, he said.

KFF Health News is a national newsroom that produces in-depth journalism about health issues and is one of the core operating programs at KFF—an independent source of health policy research, polling, and journalism. Learn more about KFF.

USE OUR CONTENT

This story can be republished for free (details).

2 years 1 month ago

Health Care Costs, Health Industry, Pharmaceuticals, Drug Costs, Kentucky, New York, Prescription Drugs, Tennessee

KFF Health News' 'What the Health?': Underinsured Is the New Uninsured

The Host

Emmarie Huetteman

KFF Health News

Emmarie Huetteman, associate Washington editor, previously spent more than a decade reporting on the federal government, most recently covering surprise medical bills, drug pricing reform, and other health policy debates in Washington and on the campaign trail.

The Host

Emmarie Huetteman

KFF Health News

Emmarie Huetteman, associate Washington editor, previously spent more than a decade reporting on the federal government, most recently covering surprise medical bills, drug pricing reform, and other health policy debates in Washington and on the campaign trail.

The annual U.S. Census Bureau report this week revealed a drop in the uninsured rate last year as more working-age people obtained employer coverage. However, this year’s end of pandemic-era protections — which allowed many people to stay on Medicaid — is likely to have changed that picture quite a bit since. Meanwhile, reports show even many of those with insurance continue to struggle to afford their health care costs, and some providers are encouraging patients to take out loans that tack interest onto their medical debt.

Also, a mystery is unfolding in the federal budget: Why has recent Medicare spending per beneficiary leveled off? And the CDC recommends anyone who isat least 6 months old get the new covid booster.

This week’s panelists are Emmarie Huetteman of KFF Health News, Margot Sanger-Katz of The New York Times, Sarah Karlin-Smith of the Pink Sheet, and Joanne Kenen of the Johns Hopkins Bloomberg School of Public Health and Politico.

Panelists

Sarah Karlin-Smith

Pink Sheet

Joanne Kenen

Johns Hopkins Bloomberg School of Public Health and Politico

Margot Sanger-Katz

The New York Times

Among the takeaways from this week’s episode:

- The Census Bureau reported this week that the uninsured rate dropped to 10.8% in 2022, down from 11.6% in 2021, driven largely by a rise in employer-sponsored coverage. Since then, pandemic-era coverage protections have lapsed, though it remains to be seen exactly how many people could lose Medicaid coverage and stay uninsured.

- A concerning number of people who have insurance nonetheless struggle to afford their out-of-pocket costs. Medical debt is a common, escalating problem, exacerbated now as hospitals and other providers direct patients toward bank loans, credit cards, and other options that also saddle them with interest.

- Some state officials are worried that people who lose their Medicaid coverage could choose short-term health insurance plans with limited benefits — so-called junk plans — and find themselves owing more than they’d expect for future care.

- Meanwhile, a mystery is unfolding in the federal budget: After decades of warnings about runaway government spending, why has spending per Medicare beneficiary defied predictions and leveled off? At the same time, private insurance costs are increasing, with employer-sponsored plans expecting their largest increase in more than a decade.

- And the push for people to get the new covid booster is seeking to enshrine it in Americans’ annual preventive care regimen.

Plus, for “extra credit,” the panelists suggest health policy stories they read this week that they think you should read, too:

Emmarie Huetteman: KFF Health News’ “The Shrinking Number of Primary Care Physicians Is Reaching a Tipping Point,” by Elisabeth Rosenthal.

Sarah Karlin-Smith: MedPage Today’s “Rural Hospital Turns to GoFundMe to Stay Afloat,” by Kristina Fiore.

Joanne Kenen: ProPublica’s “How Columbia Ignored Women, Undermined Prosecutors and Protected a Predator for More Than 20 Years,” by Bianca Fortis and Laura Beil.

Margot Sanger-Katz: Congressional Budget Office’s “Raising the Excise Tax on Cigarettes: Effects on Health and the Federal Budget.”

Also mentioned in this week’s episode:

- U.S. Census Bureau’s “Health Insurance Coverage of U.S. Workers Increased in 2022,” by Rachel Lindstrom, Katherine Keisler-Starkey, and Lisa Bunch.

- The Commonwealth Fund’s “Can Older Adults with Employer Coverage Afford Their Health Care?” by Lauren A. Haynes and Sara R. Collins.

- KFF Health News’ “What One Lending Company’s Hospital Contracts Reveal About Financing Patient Debt,” by Noam N. Levey.

- The New York Times’ “A Huge Threat to the U.S. Budget Has Receded. And No One Is Sure Why,” by Margot Sanger-Katz, Alicia Parlapiano, and Josh Katz.

- The Wall Street Journal’s “Health-Insurance Costs Are Taking Biggest Jumps in Years,” by Anna Wilde Mathews.

- The New York Times’ “The N.Y.C. Neighborhood That’s Getting Even Thinner on Ozempic,” by Joseph Goldstein.

click to open the transcript

Transcript: Underinsured Is the New Uninsured

KFF Health News’ ‘What the Health?’

Episode Title: Underinsured Is the New Uninsured

Episode Number: 314

Published: Sept. 14, 2023

[Editor’s note: This transcript, generated using transcription software, has been edited for style and clarity.]

Emmarie Huetteman: Hello and welcome back to “What the Health?” I’m Emmarie Huetteman, a Washington editor for KFF Health News. I’m filling in for Julie [Rovner] this week, who’s on vacation. And I’m joined by some of the best and smartest health reporters in Washington. We’re taping this week on Thursday, Sept. 14, at 11 a.m. As always, news happens fast, and things might have changed by the time you hear this. So, here we go. We’re joined today by video conference by Margot Sanger-Katz of The New York Times.

Margot Sanger-Katz: Good morning, everybody.

Huetteman: Sarah Karlin-Smith of the Pink Sheet.

Sarah Karlin-Smith: Hi there.

Huetteman: And Joanne Kenen of the Johns Hopkins Bloomberg School of Public Health and Politico.

Joanne Kenen: Hi, everybody.

Huetteman: No interview this week, so let’s get right to the news. The percentage of working-age adults with health insurance went up last year, according to the annual Census report out this week. As a result, the uninsured rate dropped to 10.8% in 2022. But lower uninsured rates may be obscuring another problem: the number of people who are underinsured and facing high out-of-pocket costs. The Commonwealth Fund released a report last month on how difficult it is for many older adults with employer coverage to afford care. And recent reporting here at KFF Health News has probed how medical providers are steering patients toward bank loans and credit cards that saddled them with interest on top of their medical debt. So, the number of people without insurance is dropping. But that doesn’t mean that health care is becoming more affordable. So what does it mean to be underinsured? Are the policy conversations that focus on the uninsured rate missing the mark?

Sanger-Katz: So, two things I would say. One is that I even think that the Census report on what’s happening with the uninsured is obscuring a different issue, which is that there’s been this artificial increase in the number of people who are enrolled in Medicaid as a result of this pandemic policy. So the Congress said to the states, if you want to get extra money for your Medicaid program through the public health emergency, then you can’t kick anyone out of Medicaid regardless of whether they are no longer eligible for the program. And that provision expired this spring. And so this is one of the big stories in health policy that’s happening this year. States are trying to figure out how to reevaluate all of these people who have been in their Medicaid program for all these years and determine who’s eligible and who’s not eligible. And there’s been quite a lot of very good reporting on what’s going on. And I think there’s a combination of people who are losing their Medicaid coverage because they really genuinely are no longer eligible for Medicaid. And there also appears to be quite a large number of people who are losing their Medicaid coverage for administrative hiccup reasons — because there’s some paperwork error, or because they moved and they didn’t get a letter, or some other glitch in the system. And so when I looked at these numbers on the uninsured rate, in some ways what it told us is we gave a whole bunch of people insurance through these public programs during the pandemic and that depressed the uninsured rate. But we know right now that millions of people have lost insurance, even in the last few months, with more to come later this year. And so I’m very interested in the next installment of the Census report when we get back to more or less a normal Medicaid system, how many people will be without insurance. So that’s just one thing. And then just to get to your question, I think having insurance does not always mean that you can actually afford to pay for the health care that you need. We’ve seen over the last few decades a shift towards higher-deductible health care plans where people have to pay more money out-of-pocket before their insurance kicks in. We’ve also seen other kinds of cost sharing increase, where people have to pay higher copayments or a percentage of the cost of their care. And we’ve also seen, particularly in the Obamacare exchanges, but also in the employer market, that there’s a lot of insurance that doesn’t include any kind of out-of-network benefit. So it means, you know, if you can go to a provider who is covered by your insurance, your insurance will pay for it. But if you can’t find someone who’s covered by your insurance, you could still get hit with a big bill. The sort of surprise bills of old are banned. But, you know, the doctor can tell you in advance, and you can go and get all these medical services and then end up with some big bills. So whether or not just having an insurance card is really enough to ensure that people have access to health care remains an open question. And I think we have seen a lot of evidence over recent years that even people with insurance encounter a lot of financial difficulties when they get sick and often incur quite a lot of debt despite having insurance that protects them from the unlimited costs that they might face if they were uninsured.

Huetteman: Joanne.

Kenen: I would say two big things. The uninsurance rate, which we all think is going to go up because of this Medicaid unwinding, it’s worth stopping and thinking about. It’s what? 7.9[%]? Was that the number?

Huetteman: It was 10.8, was the uninsured rate last year.

Sanger-Katz: It depends if you look at any time of the year or all of the year.

Kenen: Back when the ACA [Affordable Care Act] was passed, it was closer to something like 18. So in terms of really changing the magnitude of the uninsurance problem in America, the work isn’t done. But this is a really significant change. Secondly, some aspects of care are better — or within reach because the ACA made so many preventive and primary care services free. That, too, is a gain. Obviously, through the medical debt, which KFF [Health News] now has done a great job — oh, and believe me, and other reporters, you’ve done an amazing job, story after story. You know, the “Bill of the Month” series that you edited, it’s … but they’re not isolated cases. It’s not like, oh, this person ran into this, you know, cost buzz saw. There’s insane pricing issues! And out-of-pocket and, you know, deductibles and extras, and incredibly hard to sort out even if you are a sophisticated, insured consumer of health care. Pricing is a mess. There have been changes to the health care market, in terms of consolidation of ownership, more private equity, bigger entities that just have created … added a new dimension to this problem. So have we made gains? We’ve made really important gains. Under the original ACA passed under the Obama administration and the changes, the access and generosity of subsidy changes that the Biden administration has made, even though they’re time-limited, they have to be renewed. But, you know, are people still being completely hit over the head and every other body part by really expensive costs? Yes. That is still a heartbreaking and really serious problem. I mean, I can just give one tiny incident where somebody … I needed a routine imaging thing in network. The doctor in that hospital wasn’t reachable. I had my primary care person send in the order because she’s not part of that health care system. She’s in network. The imaging center is in network. The doctor who told me I needed this test is in network. But because the actual order came from somebody not in their hospital and in … on the Maryland side of the line, instead of the D.C. side of the line, the hospital imaging center decided it was going to be out of network. And because she’s not ours and wanted to charge me an insane amount of money. I sorted it out. But it took me an insane amount of time and I shouldn’t have needed to do that.

Huetteman: Yeah, that’s absolutely true.

Kenen: I could have paid it, if I had to.

Huetteman: Absolutely. And as you noted, I do edit the “Bill of the Month” series. And we see that with all kinds of patients, even the most enterprising patients can’t get an answer to simple questions like, is this in network or out of network? Why did I get this bill? And it’s asking way too much of most people to try and fit that into the rest of the things that they do every day. You know, Margot brought up the Medicaid unwinding. Well, let’s speaking of insurance, let’s catch up there for a moment because there was a little news this week. We’re keeping an eye on those efforts to strip ineligible beneficiaries from state Medicaid rolls since the covid-19 public health emergency ended. Now, some state officials are worried that people who lose coverage could opt to replace it with short-term insurance plans. You might know them as “junk plans.” They often come with lower price tags, but these short-term plans do not have to follow the Affordable Care Act’s rules about what to cover. And people in the plans have found themselves owing for care they thought would be covered. The Trump administration expanded these plans, but this summer the Biden administration proposed limiting them once more. Remind us: What changes has Biden proposed for so-called junk plans and for people who lose their coverage during the Medicaid unwinding? What other options are available to them?

Sanger-Katz: So the Biden administration’s proposal was to basically return these short-term plans to actual short-term coverage, which is what they were designed to do. Part of what the Trump administration did is they kept this category of short-term plans. But then they said basically, well, you can just keep them for several years. And so they really became a more affordable but less comprehensive substitute for ACA-compliant insurance. So the Biden administration just wants to kind of squish ’em back down and say, OK, you can have them for like a couple of months, but you can’t keep them forever. I will say that a lot of people who are losing their Medicaid coverage as a result of the unwinding are probably pretty low on the income scale, just as a result of them having qualified for Medicaid in the first place. And so a very large share of them are eligible for free or close-to-free health plans on the Obamacare exchanges. Those enhanced subsidies that Joanne mentioned, they’re temporary, but they’re there for a few years. They really make a big difference for exactly this population that’s losing Medicaid coverage. If you’re just over the poverty line, you can often get a free plan that’s a — this is very technical, but — it’s a silver plan with these cost-sharing wraparound benefits. And so you end up with a plan where you really don’t have to pay very much at the point of care. You don’t have to pay anything in a premium. So I think, in general, that is the most obvious answer for most of these people who are losing their Medicaid. But I think it is a challenge to navigate that system, for states to help steer people towards these other options, and for them to get enrolled in a timely way. Because, of course, Obamacare markets are not open all the time. They’re open during an open enrollment period or for a short period after you lose another type of coverage.

Huetteman: Absolutely. And a lot of these states actually have efforts that are normally focused on open enrollment right now. And some officials say that they are redirecting those efforts toward helping these folks who are losing their Medicaid coverage to find the options, like those exchange plans that are available for zero-dollar premiums or low premiums under the subsidies available.

Kenen: I have seen some online ads from HHS [the Department of Health and Human Services], saying, you know, “Did you lose your Medicaid?” and it’s state-specific — “Did you lose your Medicaid in Virginia?” I don’t live in Virginia, so I’m not sure why I’m getting it. My phone is telling me the Virginia one. But there is an HHS [ad], and it is saying if you lost your Medicaid, go to healthcare.gov, we can help. You know, we may be able to help you. So they are outreaching, although I’m afraid that somebody who actually lost it in Virginia might be getting an ad about Nebraska or whatever. I live close to Virginia. It’s close enough. But there is some effort to reach people in a plain English, accessible pop-up on your phone, or your web browser, kind of way. So I have seen that over the last few weeks because the special enrollment period, I mean, most people who are no longer eligible for Medicaid are eligible for something, and something other than a junk plan. Some of them have insurance at work now because the job market is better than it was in 2020, obviously. Many people will be eligible for these highly subsidized plans that Margot just talked about. Very few people should be left out in the cold, but there’s a lot of work to be done to make those connections.

Huetteman: Absolutely. Absolutely. And going back to the Census report for a second, it had noted that a big part of the increase in coverage came from employer-sponsored coverage among working-age adults, although we have, of course, seen those reports that say … and then they try to afford their health care costs. And it’s really difficult for a lot of them, even when they have that insurance, as we talked about. All right. So let’s move on. The New York Times is reporting a mystery unfolding in the federal budget. And I’d like to call it “The Case of Flat Medicare Spending.” After decades of warnings about runaway government spending, a recent Times analysis shows that spending per Medicare beneficiary has actually leveled off over more than a decade. Meanwhile, The Wall Street Journal reports that private health insurance costs are climbing. Next year, employer-sponsored plans could see their biggest cost increase in more than a decade, and that trend could continue. So what’s going on with insurance costs? Let’s start with Medicare. Margot, you were the lead reporter on the Times analysis. What explains this Medicare spending slowdown?